En

l état en l état scholarships.

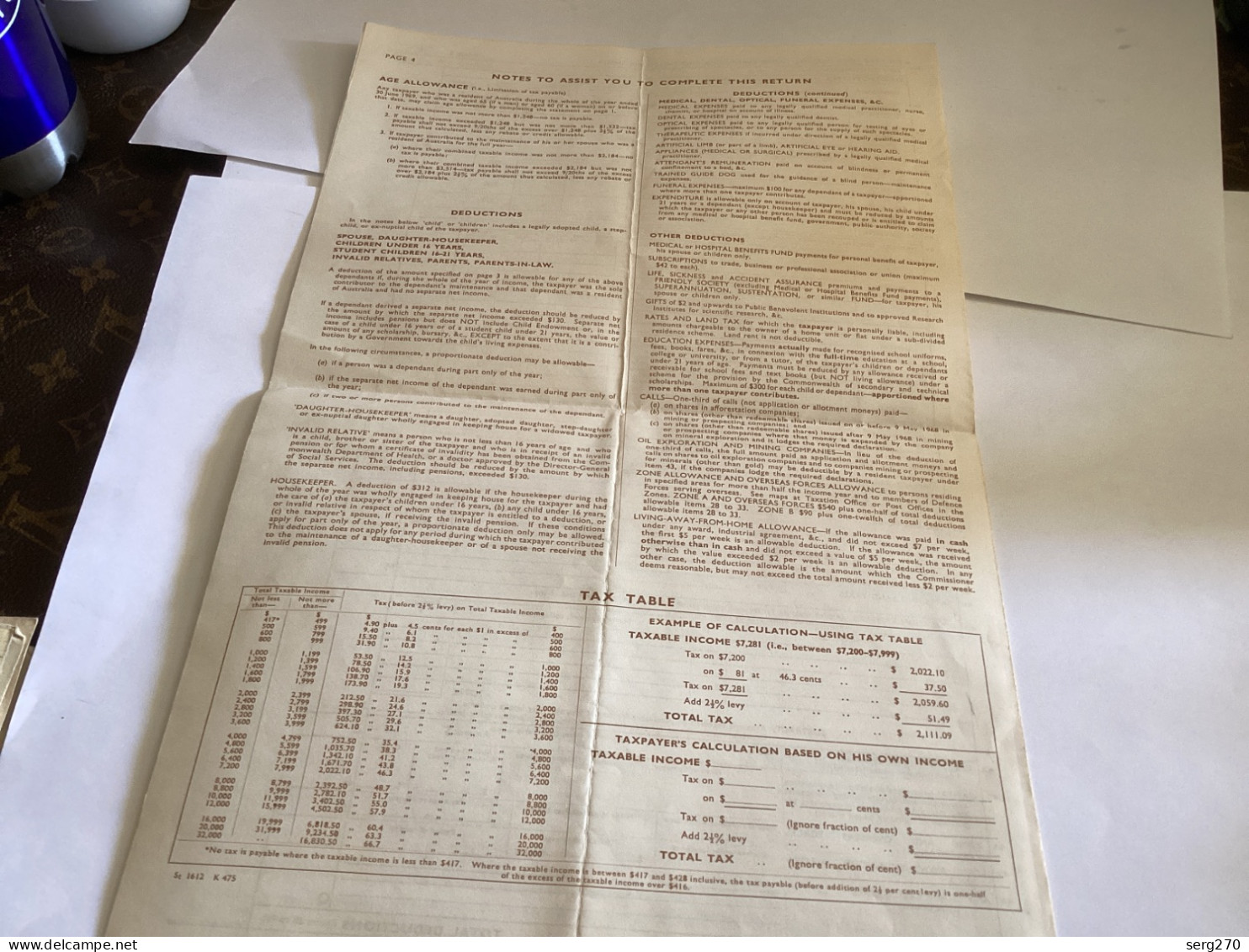

Maximum of $300 for each child or dependant-apportioned where

more than one taxpayer contributes.

CALLS- One-third of calls (not application or allotment moneys) paid-

8) on shares in afforestation companies;

on shares (other than redomable shares) issued on or before 9 May 1968 in mining

(e) anshares Pother char companisi:

redeemable shares) issued after 9 May. 1968 in mining

or prospecting,

coRIPantes where chat money is expended by the company

on mineral exploration and it lodges the required declaration.

OIL

EXPLORATION

AND

MINING

COMPANIES- In lieu of the deduction of

one-third of calls, the full amount paid as application and allotment moneys and calls on shares to oil exploration companies and to companies mining or prospecting for minerals (other than gold) may be deductible by a resident taxpayer under item 43, if the companies lodge the required declarations.

ZONE ALLOWANCE AND OVERSEAS FORCES ALLOWANCE to persons residing in specified areas for more than half the income year and to members of Defence

Forces serving overseas..

See maps at

Zones.

Taxation Office or Post Offices in the

ZONE A AND OVERSEAS FORCES $540 plus one-half of total deductions

allowable items 28 to 33. allowable items 28 to 33.

ZONE B $90 plus one-twelfth of total deductions

LIVING-AWAY-FROM-HOME ALLOWANCE-_If the allowance was paid in cash under any award, industrial agreement, &c., and did not exceed $7 per week, the first $5 per week is an allowable deduction.

If the allowance was received

otherwise than in cash and did not exceed a value of $5 per week, the amount by which the value exceeded $2 per week is an allowable deduction. In any other case, the deduction allowable is the amount which the Commissioner deems reasonable, but may not exceed the total amount received less $2 per week.DEDUCTIONS

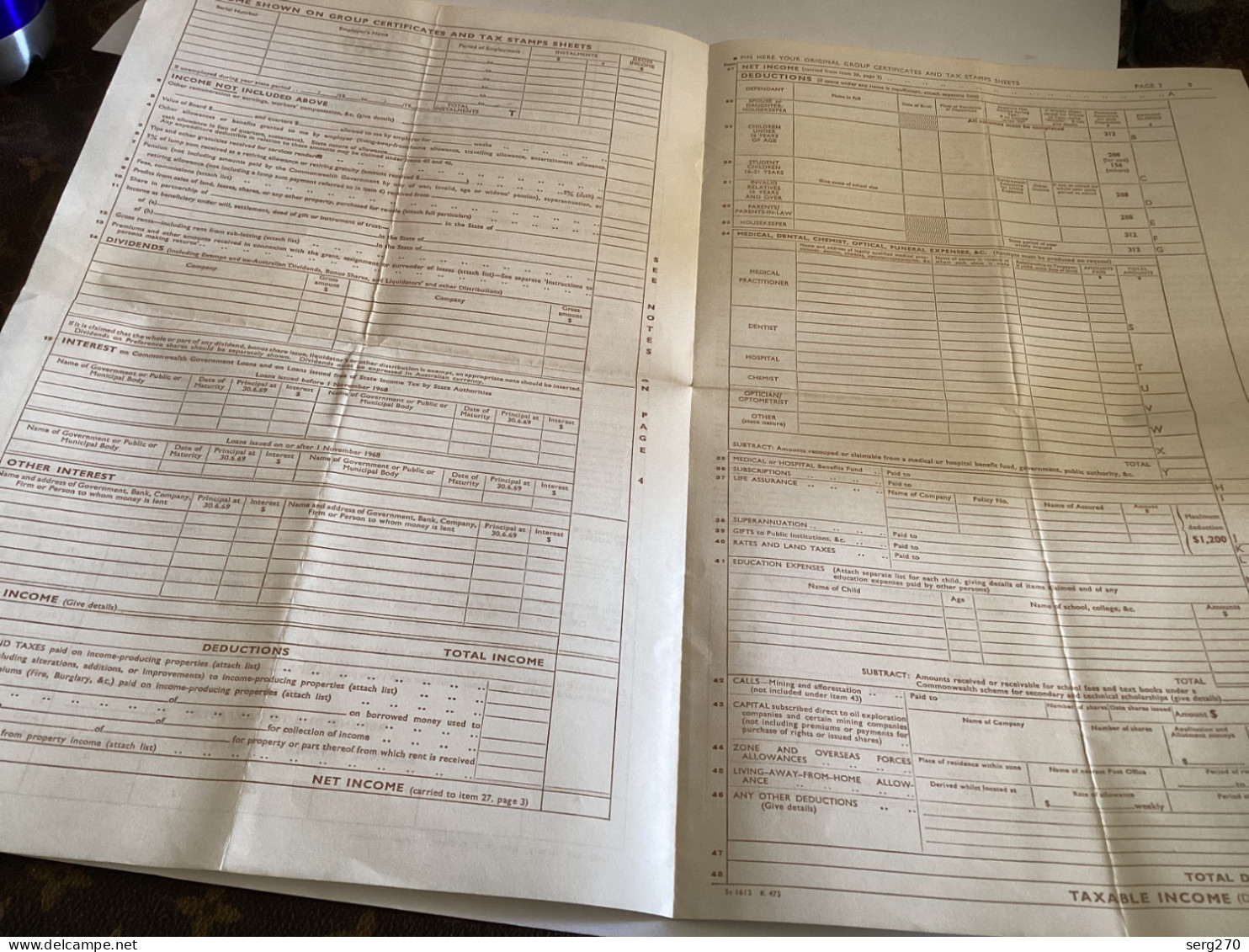

In the notes below 'child' or 'children' includes a legally adopted child, a step-child, or ex-nuptial child of the taxpayer.

SPOUSE, DAUGHTER-HOUSEKEEPER, CHILDREN UNDER 16 YEARS, STUDENT CHILDREN 16-21 YEARS, INVALID RELATIVES, PARENTS, PARENTS-IN-LAW.

A deduction of the amount specified on page 3 is allowable for any of the above dependants if, during the whole of the year of income, the taxpayer was the sole contributor to the dependant's maintenance and that dependant was a resident of Australia and had no separate net income.NOTES TO ASSIST YOU TO COMPLETE THIS RETURN

AGE ALLOWANCE (.... Limitation of tax payable)

DEDUCTIONS (continued)

and who

was a resident of Australla during the whole of the year ended

MEDICAL, DENTAL, , OPTICAL, FUNERAL EXPENSES, &C.

legally qualified medical practitioner, nurse.

ras aged 65 (if a man) or aged

that date. may claim age allowance

60 (if a woman) on or before

MEDICAL EXPENSES paid

by completing the statement on page

chemist, or hospital on iccount or iliness.

J. If taxable income was not more than $1.248- no tax is payable.

DENTAL EXPENSES paid to any legally qualified dentist.

2. If taxable income

OPTICAL EXPENSES paid to any legally qualified person for testing of

eyes

Or

exceeden

payable shall

$1.248

but was not more.

chon

$1,532-tax

not exceed 9/20chs of the excess over

amount thus calculated. less any rebace or

248 plus 27% of the

prescribing of spectacles, or to any person for the supply of such spectacles.

credit allowable.

THERAPEUTIC EXPENSES If incurred under direction of a legally qualified medical

3. Fesaxpayer contributed to the maintainance of his or her spouse who was a

Australia for the full year-

ARTIFICIAL LIMB (or part of a limb), ARTIFICIAL EYE or HEARING AID.

(a) where their combined taxable income was not more than $2,184-no

APPLIANCES (MEDICAL OR SURGICAL) prescribed by a legally qualified medical

tax is payable;

practitioner.

ATTENDANT'S REMUNERATION paid on account of blindness or permanent

(b) where their combined taxable income exceeded $2,184 but was not

confinement to a bed, &c.

than $3,514 tax payable shall not exceed 9/20ths of the excess

TRAINED GUIDE DOG used for the guidance of a blind person-

-maintenance

over $2,184 plus 21% of the amount thus calculated, less any rebate or credit allowable.

expenses.

FUNERAL EXPENSES- -maximum $100 for any dependant of a taxpayer--apportioned

where more than one taxpayer contributes.

EXPENDITURE is allowable only on account of taxpayer, his spouse, his child under 21 years or a dependant (except housekeeper) and must be reduced by amounts which the taxpayer or any other person has been recouped or is entitled to claim from any medical or hospital benefit fund, government, public authority, society

DEDUCTIONS

or association.

e notes below 'child' or 'children' includes a legally adopted child, a step-ex-nuptial child of the taxpayer.

; DAUGHTER-HOUSEKEEPER, IN UNDER 16 YEARS,

OTHER DEDUCTIONS

MEDICAL or HOSPITAL BENEFITS FUND payments for personal benefit of taxpayer, his spouse or children only.

ALISeADIOTIONS ta trade.

business or professional association or union (maximurNEW SOUTH WALES

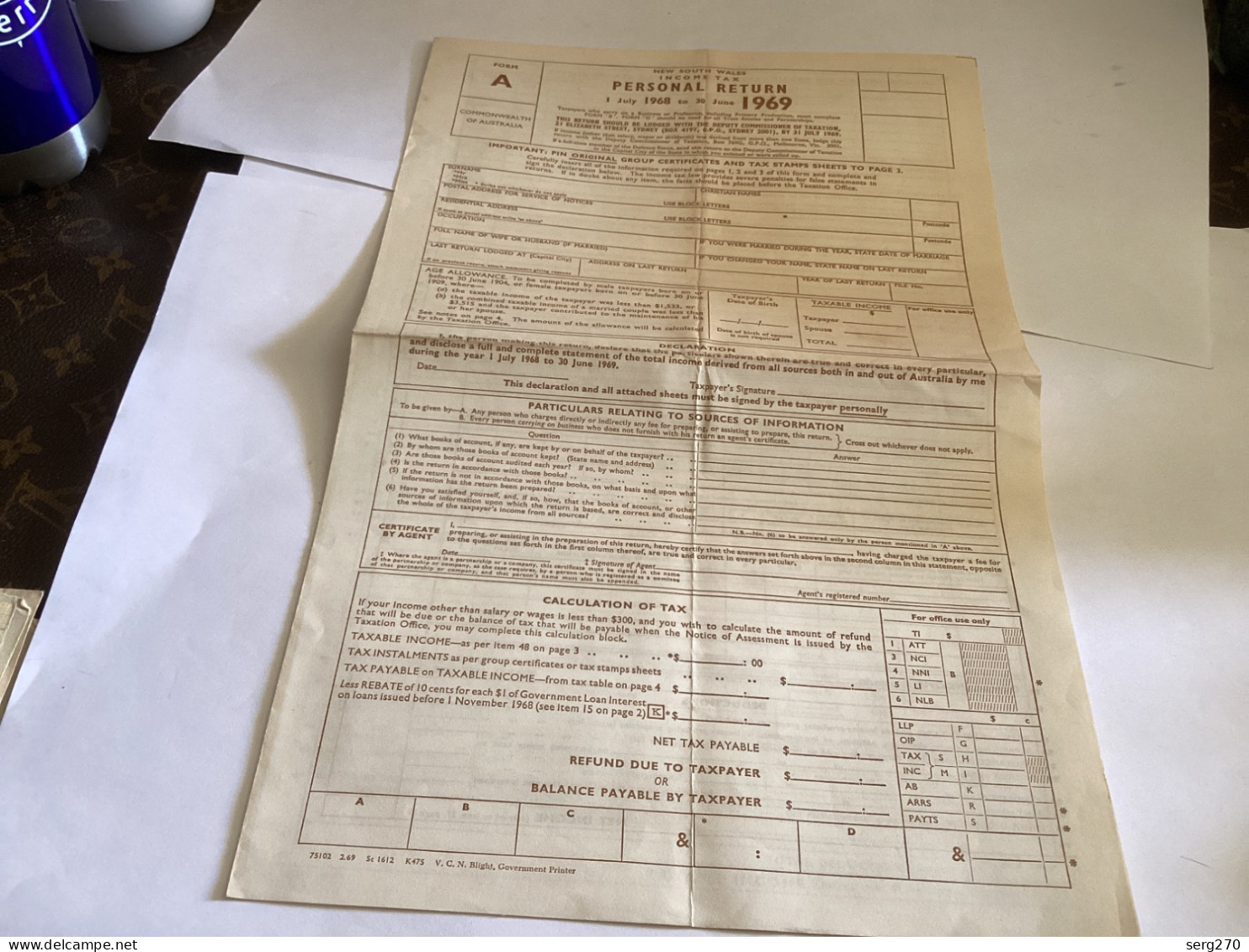

FORM

A

INCOME

TAX

PERSONAL RETURN

I July 1968 to 30 June

June [969

Taxpayer oki carry On Business on frofession, oncludingust isstates and "fartherships.complete

should be used for all Trust Estates and Partnerships.

COMMONWEALTH

OF AUSTRALIA

THIS RETURN SHOULD BE LODGED WITH THE DEPUTY COMMISSIONER OF TAXATION,

21 ELIZABETH STREET, SYDNEY (BOX 4197, G.P.O, SYDNEY 2001), BY 31 JULY 1969.

Focacome Cather that salary, mases on divide nde. ten debo a 65am, m re thielbouras, Vid st.

G.P.O., Melbourne,

If a full-time member of the Defence Force, send this return to the Deputy Commissioner of Taxation in the Capital City of the State in which you enlisted or were called up.

IMPORTANT: PIN ORIGINAL GROUP CERTIFICATES AND TAX STAMPS SHEETS TO PA

Carefully insert all of the information required on pages I, 2 and 3 of this form and complete and sign the declaration below.

The income tax law provides severe penalties for false statements in

returns.

If in doubt about any item, the facts should be placed before the Taxation Office.

CHRISTIAN NAMESI July 1968 to

30

Tune

Tarpayore o o? 임유

Business or Profession, Including Primary Production, must complete

for all Trust Estates and Partnerships.

COMMONWEALTH

OF AUSTRALIA

THIS RETURN SHOULD BE LODGED WITH THE DEPUTY COMMISSIONER OF TAXATION,

21 ELIZABETH STREET, SYDNEY (BOX 4197, 6.P.O., SYDNEY 2001), BY 31 JULY 1969.

wages or dividends) was derived from more than one State, lodge this

return with the Deputy

if a full-time member of the Defence Force, send this return to the Deputy Commissioner of Taxation in the Capital City of the State in which you enlisted or were called up.

IMPORTANT: PIN ORIGINAL GROUP CERTIFICATES AND TAX STAMPS SHEETS TO PAGE 3.

Carefully insert all of the information required on pages 1, 2 and 3 of this form and complete and sign the declaration below.

returns.

The income tax law provides severe penalties for false statements in

If in doubt about any item, the facts should be placed before the Taxation Office.

CHRISTIAN NAMES